This is probably one of the most frequently asked questions: What KPIs should we use for the compensation system? In this article, I’d like to review the best practices about using, or in most cases, not using reward KPIs.

I did a classification of possible approaches to the reward system. Don’t take these levels as the levels of business maturity; your goal might be not to get to Level 4 but achieve excellence on Level 2.

Any business chooses one or another reward model because of the specific business environment and the current business challenges.

There is no absolute truth about which approaches should be used.

The Need for Reward. XY Theory

The first question is, why do employees need to be rewarded?

- The reward is supposed to increase the motivation of an employee.

- Maslow’s hierarchy of needs (Maslow, 1970)

- Herzberg’s motivation-hygiene theory (Herzberg, 2003)

- McGregor XY Theory1.

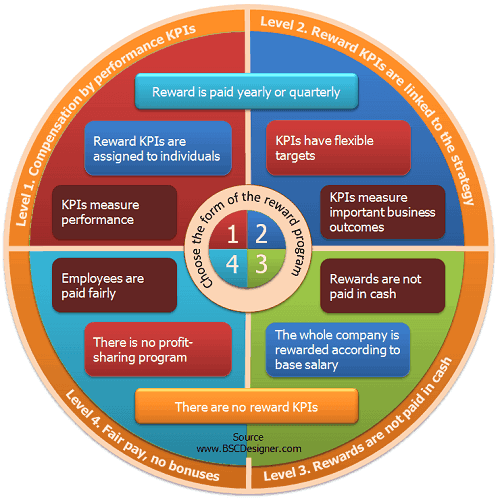

Level 1. Compensation Defined by Performance KPIs

The basic idea of linking a compensation plan to KPIs is simple.

Track the performance of our employees, and if they are performing well, give them a bonus that is supposed to motivate them to deliver even better results.

This approach has some important disadvantages:

Disadvantage: Biased Performance Measurement

Let’s take sales representatives as an example. The root-case connection between their efforts and the financial outcomes seems to be clear, but still the short-term financial outcomes should be validated by long-term business impact.

It is hard to measure the performance of the employees, especially when employees know that their bonuses depend on the results.

Companies that forget about this face situations like we reviewed in the KPIs misuse article.

Common Characteristics

- Managers follow the “Theory X” approach

- KPIs are assigned to individuals to measure their performance

- KPIs have fixed target values

- Reward is paid yearly, quarterly and/or monthly according to the KPIs

Toolkit

- Use spreadsheet software to build a prototype of reward calculations.

- Move to the professional tool for scorecard calculation once the underlying logic is stable.

Level 2. Compensation KPIs are Linked to Strategic Objectives

A better approach would be to have a properly described strategy and link reward KPIs to the company’s strategic objectives.

- In theory, this approach is better as now a compensation plan is linked to achieving strategic objectives;

- In practice, most managers still focus on short-term performance KPIs (see the “KPIs, Performance & Reward” research2) or use strategic KPIs that don’t make sense for line managers.

Disadvantage: Strategy Needs to be Cascaded First

There are two disadvantages of this approach:

- It is not clear if/how specific individuals contributed to the company’s success.

- Measuring a company’s success is an important challenge itself.

Let’s take a retail bank where top managers measure the success of their organization by Earnings per Share. This indicator depends on many factors:

- The decisions of shareholders and top managers

- The competition from FinTech companies

- The possible issues with regulators

If we link reward to this strategic KPI, it will probably make sense for top managers but won’t make any sense for the line-level managers.

What might be a solution to these challenges?

A strategic objective needs to be properly cascaded to make sense on the local level.

In the case with the bank, it will make much more sense to link reward to the “local” version of strategic goals that have some relevance to the employees that are being evaluated.

Common Characteristics

- Managers say they follow “Theory Y,” but in many cases, they continue to follow the “Theory X” approach

- KPIs track important business outcomes

- KPIs have flexible targets

- Reward is paid yearly or quarterly

Toolkit

- Use Balanced Scorecard software to formulate and cascade your strategy

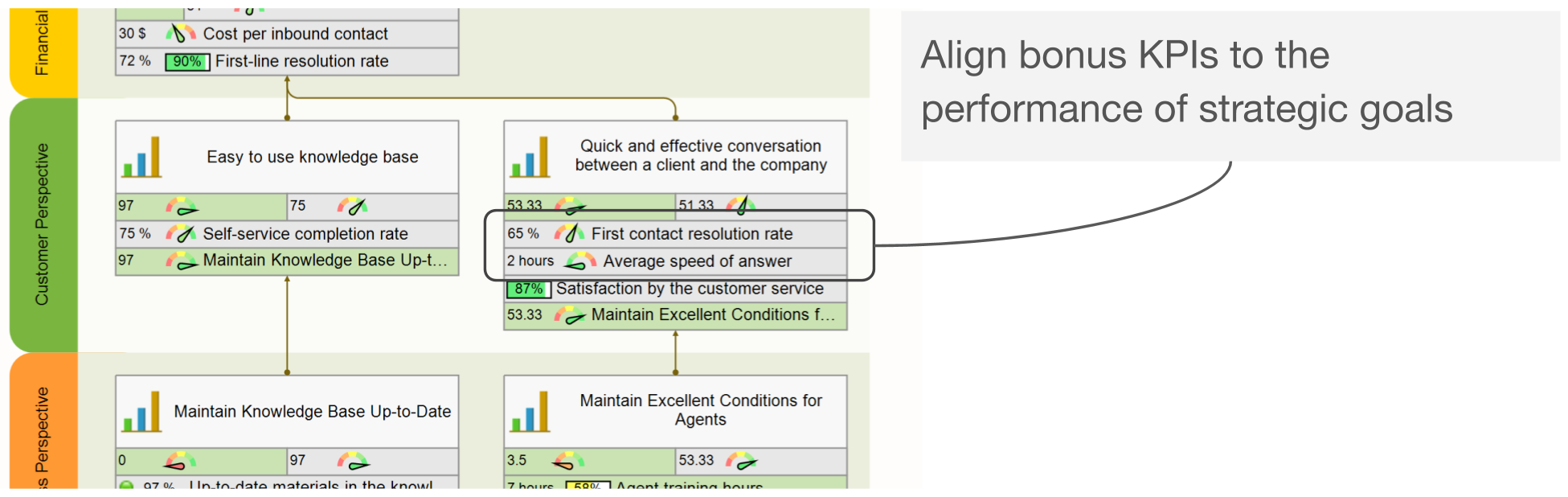

- Align bonus KPIs to the performance of strategic goals

Level 3. Rewards Are Not Paid in Cash

On this level, employees are not compensated with financial bonuses at all. The idea is that why should one be paid twice (first time with a salary and second time with a bonus) for the same job?

Jeremy Hope in “How KPIs can help motivate and reward the right behavior”3 shares an interesting example. The author quoted Herb Kelleher, Chairman of Southwest Airlines when he is speaking about employee compensation:

“If somebody was working just to be compensated, we probably didn’t want them at Southwest Airlines. We wanted them working in order to do something in an excellent way. And to serve people.”

Southwest Airlines has a bonus program, but employees won’t see funds soon as the company invests them in an employee retirement plan.

Disadvantage: Win Competition for Talents is More Difficult

Level 3 offers a compromise:

- There are no cash bonuses, so any short-term approach to game the system won’t work.

- Teams are compensated in the form of shares that by definition are linked to the financial success of the company.

A talent strategy of the company is never isolated from the market. If cash bonuses are traditionally paid for a certain role, then it might be hard for your organization to shift from Level 2 to Level 3.

- Be ready to see the decrease in your talent hire and retention indicators. Compensate them with higher engagement.

Common Characteristics

- Managers follow the “Theory Y” approach

- There are no KPIs for rewards

- The whole company is rewarded according to base salary

- Rewards are not paid in cash but are invested in the retirement plan or in the purchase of shares

Toolkit

Although there are no bonus KPIs, your team still needs to know about the goals of the organization and still need to measure their performance.

- Use Balanced Scorecard framework to track strategy execution

- Use light-weight OKR framework to focus the efforts of your team

Reward Program in Apple

In the previous article, I mentioned that Apple can afford to have a higher than industry average turnover rate and still find and retain the best talents in the industry. What about their reward system?

According to information available for the public, Apple suggests its employees stock purchase plan and product discounts. For example, in 2012, Apple was giving its employees a good discount on a new Mac and iPad. Well, this might be considered as a reward as well as an employee engagement program.

Apple’s senior executives are in the list of Top 5 best-paid. Besides base salary, they were paid compensation in the form of stock. This was done with a specific purpose: “to retain the company’s executive team during the CEO transition.” As for Apple’s CEO Tim Cook, the new initiative links Cook’s stock award to the company performance index in the Standard & Poor’s 500.

Level 4. Fair Pay, No Bonuses

Henry Mintberg, a professor at the Faculty of Management at McGill University, suggests an even more extreme point of view. In his article4 for The Wall Street Journal, he doesn’t suggest any cure to the problem of executive bonuses; he just says that “the problem is that they [executive bonuses] exist”!

The author talks about five reasons why executives should not be paid any bonuses. As a possible alternative, he names paying bonuses to all employees according to their base pay (similar to what was discussed on Level 3) but still sees that there is a possible problem as performance can never be evaluated correctly taking into account a long-term perspective.

It is obvious that to be able to operate on this level, a company needs to have a strong leadership 100% focused on the “Theory Y” way of working with employees. Also, the company should have an established brand among potential candidates to be able to afford to filter out employees that are motivated mostly by compensation plans.

How are the employees motivated then?

The organizations on Level 4 are shifting from extrinsic motivation (Levels 1-3) to the intrinsic ones. According to Kenneth Thomas5, there are four intrinsic rewards:

- Sense of meaningfulness. Understanding the purpose. A mission statement on the strategy map should help with this.

- Sense of choice. The employee understands the goal and can choose the best way to achieve it. On the level of strategy description, this means that the strategy is a product of discussion on each level, not just the set of goals mandated from top managers.

- Sense of competence. A sense of high-quality work done. Before, we discussed how a company can quantify and measure quality.

- Sense of progress. A sense of moving in the right direction. That’s probably the best way the KPIs can be used.

These four will look very familiar for those who estimated employee engagement using the Q12 index.

Disadvantage: You Are Testing the Water

Similar to Level 3, you might find out that your innovative reward practices are not shared by your industry colleagues.

- You’ll need to break many mental barriers of managers, HRs, and employees.

- You’ll need to find the fair salary level that can be justified to the board and attracts enough candidates to your hiring funnel.

- Your team will need to do the intrinsic motivation seriously (See the tools section below for some tips).

Common Characteristics

- Leadership according to the “Theory Y” approach

- There are no extrinsic reward KPIs

- The company focuses on the intrinsic reward KPIs

- There is no compensation or profit-sharing programs

- Employees are paid fairly, no additional bonuses are paid

Toolkit

- Continue using Balanced Scorecard and OKR frameworks as discussed in Level 3

- Work on your quality and innovation systems to give a sense of competence

- Work on your performance measurement culture to give a sense of progress

How Can BSC Designer Help?

Here are some typical scenarios of how BSC Designer software can help in terms of reward and performance calculation.

- Level 1. Use BSC Designer as an alternative to Excel, especially if you have some complex scorecard calculations with different measurement scales, normalization, weights, various performance functions.

- Level 2. Use BSC Designer to create your Balanced Scorecard and map business goals into the four perspectives. Link to the lagging indicators to get the performance figures for bonus calculation.

- Level 3. Cascade strategy across your organization and align top-level goals from Balanced Scorecard with local-level goals from light-weight OKRs.

- Level 4. Use BSC Designer to track strategy execution, including its quality and innovations aspects.

Where is the Golden Mean?

As we can see, there are different approaches to compensation programs.

- There are companies like Apple that follow a traditional model and can afford this.

- There are organizations like Southwest Airlines that prefer to focus on retaining people that are not looking for bonuses.

The executive compensation practice might be something that doesn’t help or even makes damage (See ideas by Henry Mintberg mentioned on Level 4), but they still are used widely.

Here are some summary thoughts regarding a reward system:

- Match the reward program with the business environment. Choose the form of the reward program according to your current business challenges.

- Link to what actually matters. Don’t link reward programs to an employee’s performance; instead, link reward programs to the tangible outcomes of strategic objectives.

- Reward teams, not individuals. Consider the shift from rewarding individuals to rewarding teams or the whole company.

- No cash rewards. Avoid rewards in the form of cash, as stock purchases work better.

Intrinsic rewards. Help your team to master intrinsic motivation and rewards.

- Douglas McGregor, The Human Side of Enterprise, 1960, McGraw-Hill ↩

- KPIs, Performance & Reward, Paula Kager, Dirk Lindenbergh, Global Equity Organization ↩

- How KPIs can help motivate and reward the right behavior, Jeremy Hope, 2013, IBM Software Business Analytics ↩

- No More Executive Bonuses!, Henry Mintzberg, 2009, The Wall Street Journal ↩

- The Four Intrinsic Rewards that Drive Employee Engagement, Kenneth Thomas, 2009 ↩

![]() CEO | Author | Speaker

CEO | Author | Speaker

BSC Designer is strategy execution software that enhances strategy formulation and execution through tangible KPIs. Our proprietary strategy implementation system reflects our practical experience in the strategy domain.