Build a solid base for discussion and execution of your organization’s strategy. Learn how to create a single-page strategy map following step-by-step guides and using examples.

Part 1. Guides:

- How to Create a Strategy Map in 8 Steps + Infographic

- Typical Mistakes

Part 2. Templates:

The term strategy map has its origin in the Balanced Scorecard (BSC) concept of the mid-1990s. Since then, strategy map became a buzzword, a synonym of any visual representation of strategy. Below, we’ll discuss the most popular approach to strategy map design based on the original K&N Balanced Scorecard.

Why Use a Strategy Map

A classical geographical map represents abstraction of the world around us. Instead of dealing with trees, rivers, and roads on the map, we deal with areas of different colors and lines. In the same way, a strategy map is abstraction of business and its strategy. This abstraction helps to focus on what’s important now.

The main purpose of a strategy map is to visualize the strategy of an organization in a specific way. In its turn, the visualization improves strategy discussion and execution.

If you ask me why you need a strategy map, I would mention these three reasons one after the other:

- Visualization -> Discussion -> Execution

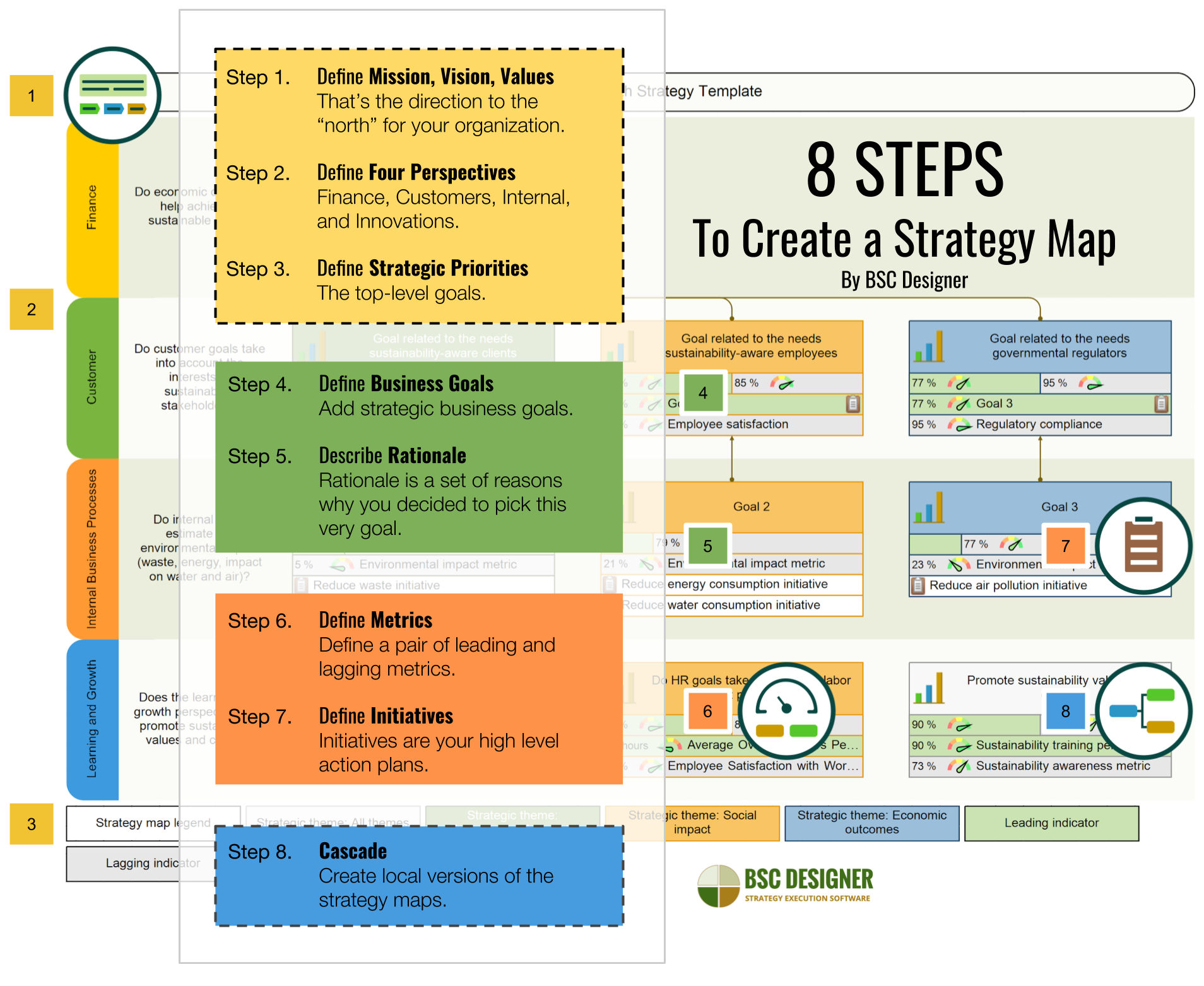

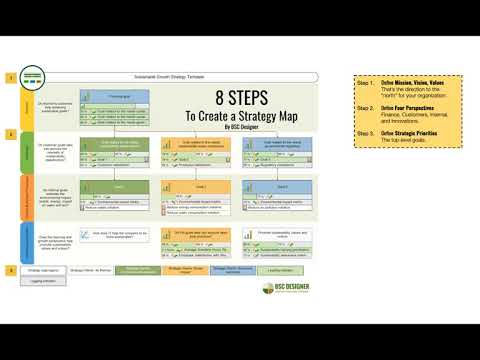

How to Create a Strategy Map

A strategy map concept comes from the K&N Balanced Scorecard. Here are key steps to creating a professional strategy map:

Step 1. Define Mission, Vision, Values

That’s the direction to the “north” for your organization. If you face uncertainty, these three will help you to make the best decisions.

Step 2. Define Four Perspectives

Finance, Customers, Internal, Innovations. You can confirm experimentally that your organization needs exactly these four. Non-profit organizations have their nuances, but the general idea is similar.

Step 3. Strategic Priorities

Strategic priorities are the top-level goals; normally, you have three main goals – serving clients better, improving operations, improving product.

Step 4. Define Business Goals

Fill in the perspectives of the strategy map with strategic business goals. There should be a cause-and-effect connection between the goals. The logic goes from top to bottom, and goals from lower perspectives explain how you plan to achieve the goals from higher perspectives.

Step 5. Describe Rationale

Rationale is a set of reasons why you decided to pick this very goal. If you use automation software, explain these reasons in the description field of the goal.

Step 6. Define Leading and Lagging Metrics

What do you mean by a business goal? The best way to answer this question is to define a pair of leading and lagging metrics with baseline and target values. Any vague goal definition becomes a specific one once performance metrics are defined.

Step 7. Define Initiatives

We mentioned “execution” as one of the purposes of the strategy map. Initiatives are your high-level action plans that explain how the strategy will be executed.

Step 8. Cascade

There should only be one top level strategy of the organization, still different business units need to focus on different parts of that strategy. Create local versions of the strategy maps with more specific goals and indicators.

If you do your first strategy map, these steps might sound like too much to assimilate. You can get started easier by using this free strategy wizard tool that will guide you through these steps and will create a strategy map for you.

Typical Mistakes of Strategy Mapping

As part of our Strategy Execution Training, we work with business professionals to create a prototype of their Balanced Scorecard strategy maps. Here are some typical mistakes that we see:

Mistake 1. Goals without Connections

The idea of the map is to show the cause-and-effect logic. If there is a goal without a connection to other goals (unless the connection is obvious), then the question is why we have that goal on the map.

Mistake 2. Focusing on Operational Goals

As mentioned before, the strategy map goals should be strategic ones. I’ve seen many cases where good strategic goals are linked to short-term binary goals like, for example, move a website to a different hosting platform.

Mistake 3. No Rationale

The choice of the goals is important; the reason for that choice is even more important. In many cases, these reasons are not explicitly described. As a result, during the next review of the strategy, it’s hard to understand why a certain goal exists on the map.

Mistake 4. Using Lagging Metrics Only

Lagging metrics help us to validate the achievement of the goal but don’t give a clue to how exactly to achieve them. Leading metrics quantify the success factors and give an answer to that question.

Mistake 5. Having a Top-Level Map Only

A top-level map won’t make a lot of sense for, let’s say, a marketing specialist who does a social media campaign. Top-level strategy needs to be aligned with the challenges of lower levels. Having a local version of a strategy map is a good idea.

Mistake 6. Having Too Many Goals

In my opinion, having more than 8-10 goals in each perspective is a red flag and a sign that the strategy was not properly cascaded. It’s like a to-do list – a list of 5-10 things works better than one of 100+ items.

Mistake 7. Mixing Goals and Metrics

“Increase sales by 15% within a year” sounds like a S.M.A.R.T. goal, but actually, it is not the best candidate for a strategy map. It’s a mix of a goal, metric, and a time frame. It won’t work for a strategy map. On step 1 of KPI template, we discussed the reasons and the solutions.

Mistake 8. Using Business Jargon

Goals like “Leverage business opportunities to satisfy customer demand” sound smart but don’t add any value to the discussion around strategy.

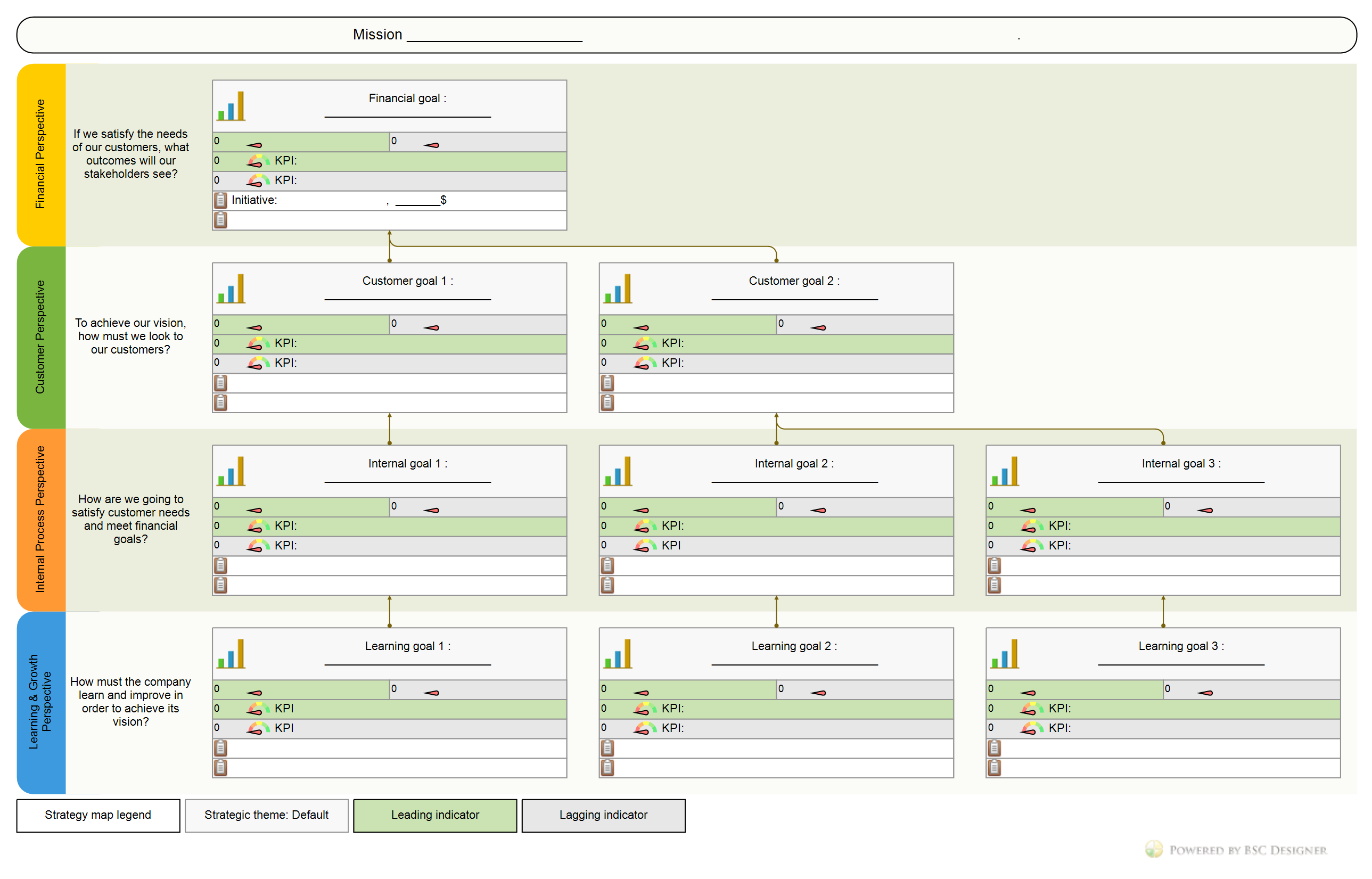

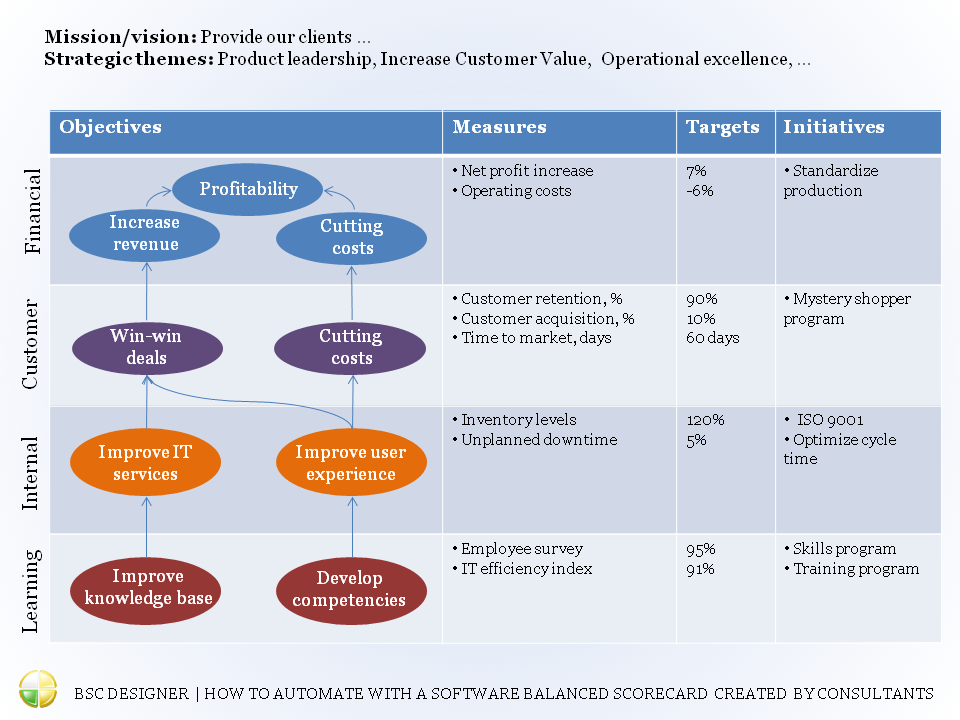

Strategy Map Template

I like the way BSC Designer software deals with strategy maps, but sometimes, it is worth using pen and paper for the brainstorming sessions. We do this on some of our live events, and I’d like to share with you a strategy map template that we use.

Download PDF | View in BSC Designer Online

Download Template

| Language | Download PDF | Open Template Online |

|---|---|---|

| English | Download PDF | Open Online |

| Spanish | Download PDF | Open Online |

| German | Download PDF | Open Online |

| Russian | Download PDF | Open Online |

| Portuguese | Download PDF | Open Online |

Getting Started Instructions

A strategy map template includes four perspectives. The rectangles inside the perspectives represent business goals.

A business goal includes several lines to fill in:

- Use the first line to formulate the name of the goal.

- Use the two lines with the “clipboard” icon to write down some initiatives and some relevant budget or timing information.

- Use the first “KPI” line to write down leading KPIs for this business goal.

- Use the second “KPI” line to write down lagging KPIs for the business goal.

Once you’ve sorted out the ideas about your strategy, go ahead and automate goals, initiatives, and KPIs with the BSC Designer tool.

Strategy Map Examples

Find below some examples of the strategy maps created with BSC Designer Online. You can sign-up with a free account and get immediate access to those templates.

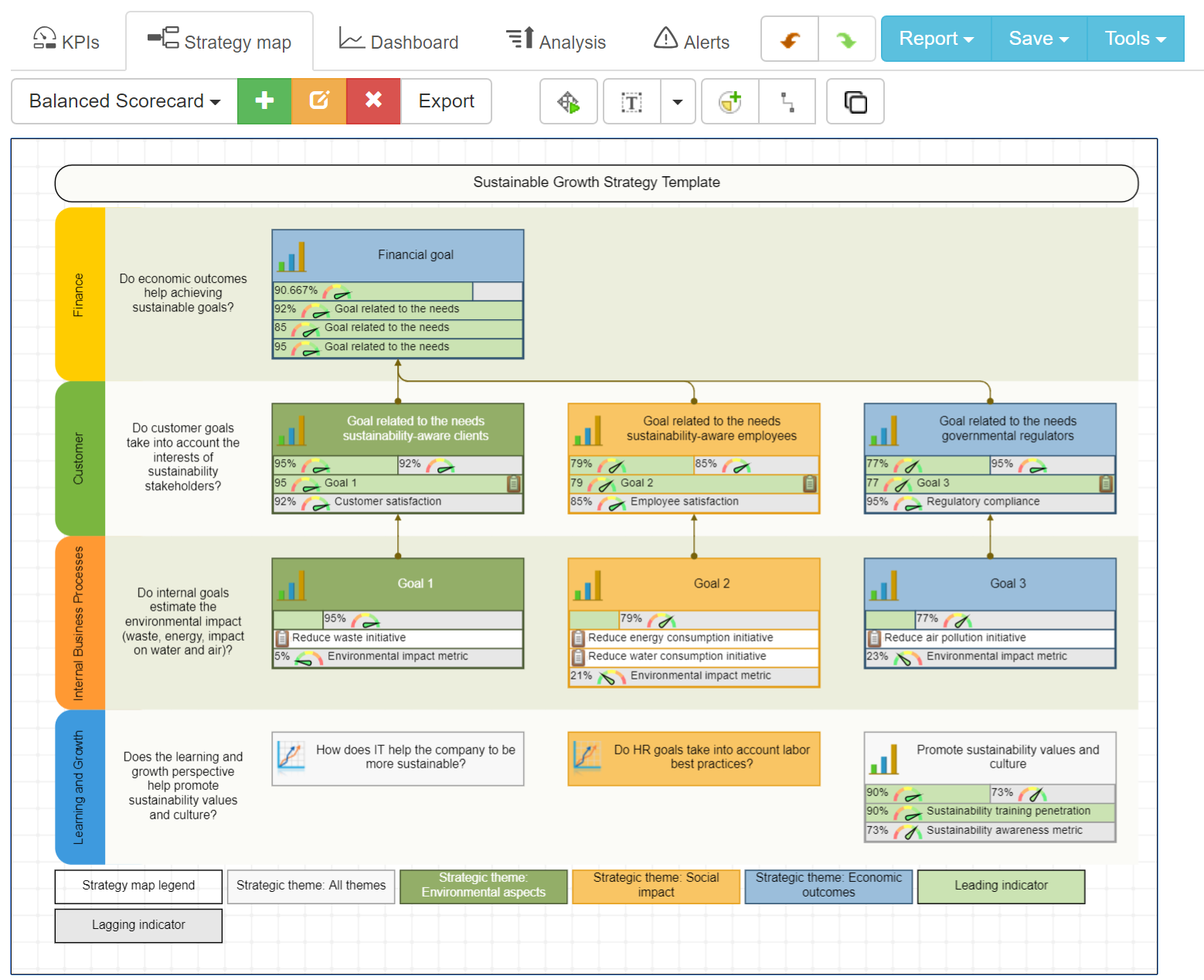

Sustainable Strategy Map Template

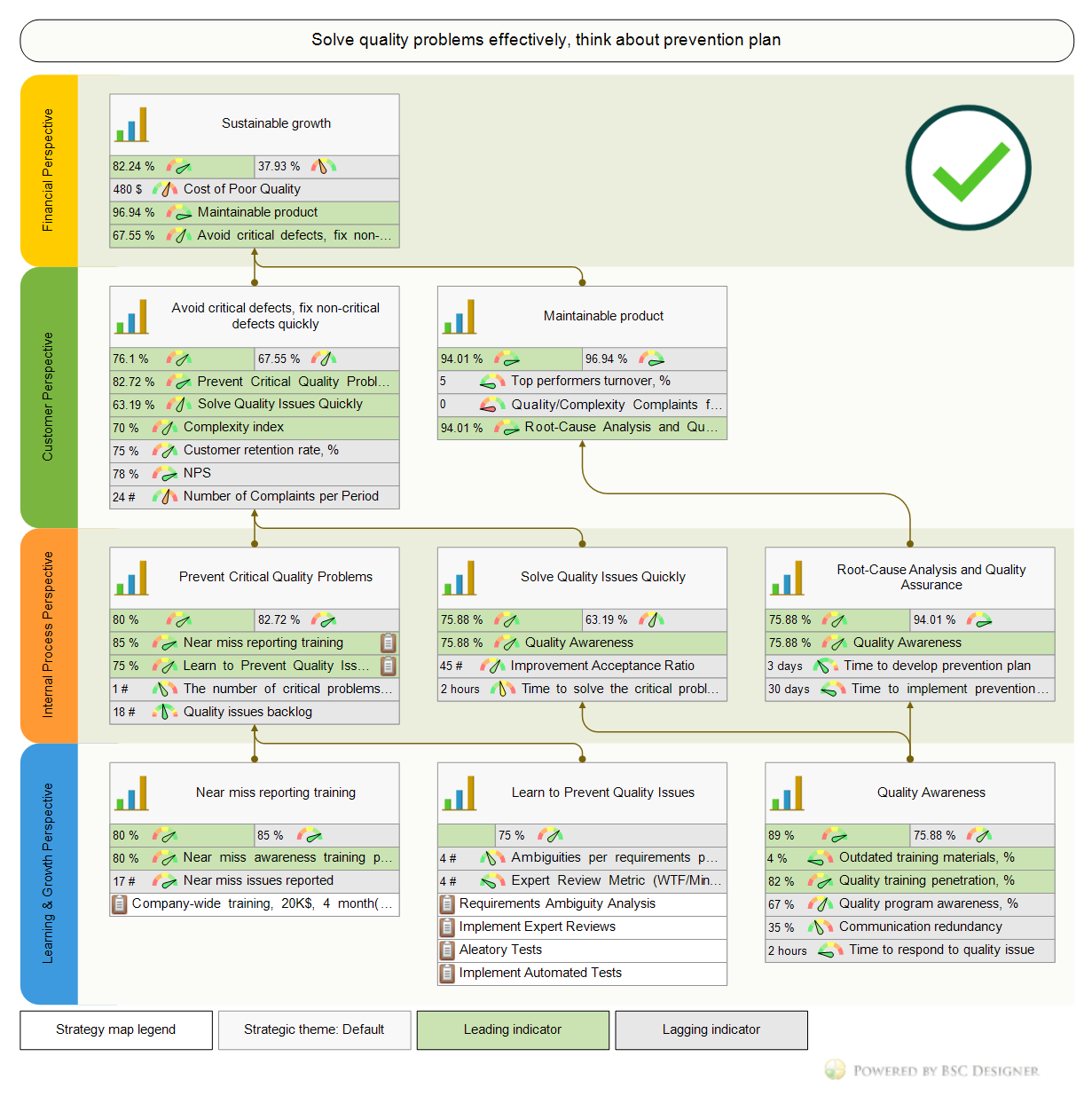

Quality Strategy Map Template

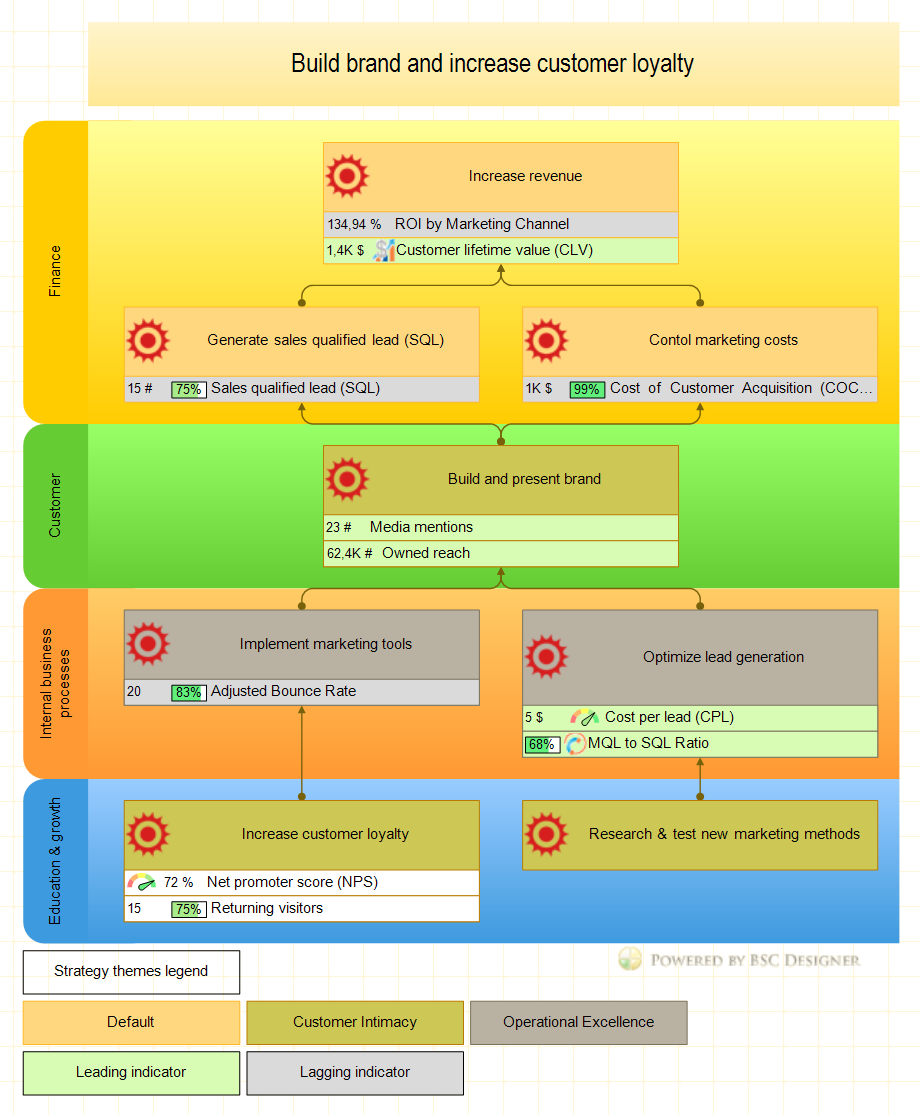

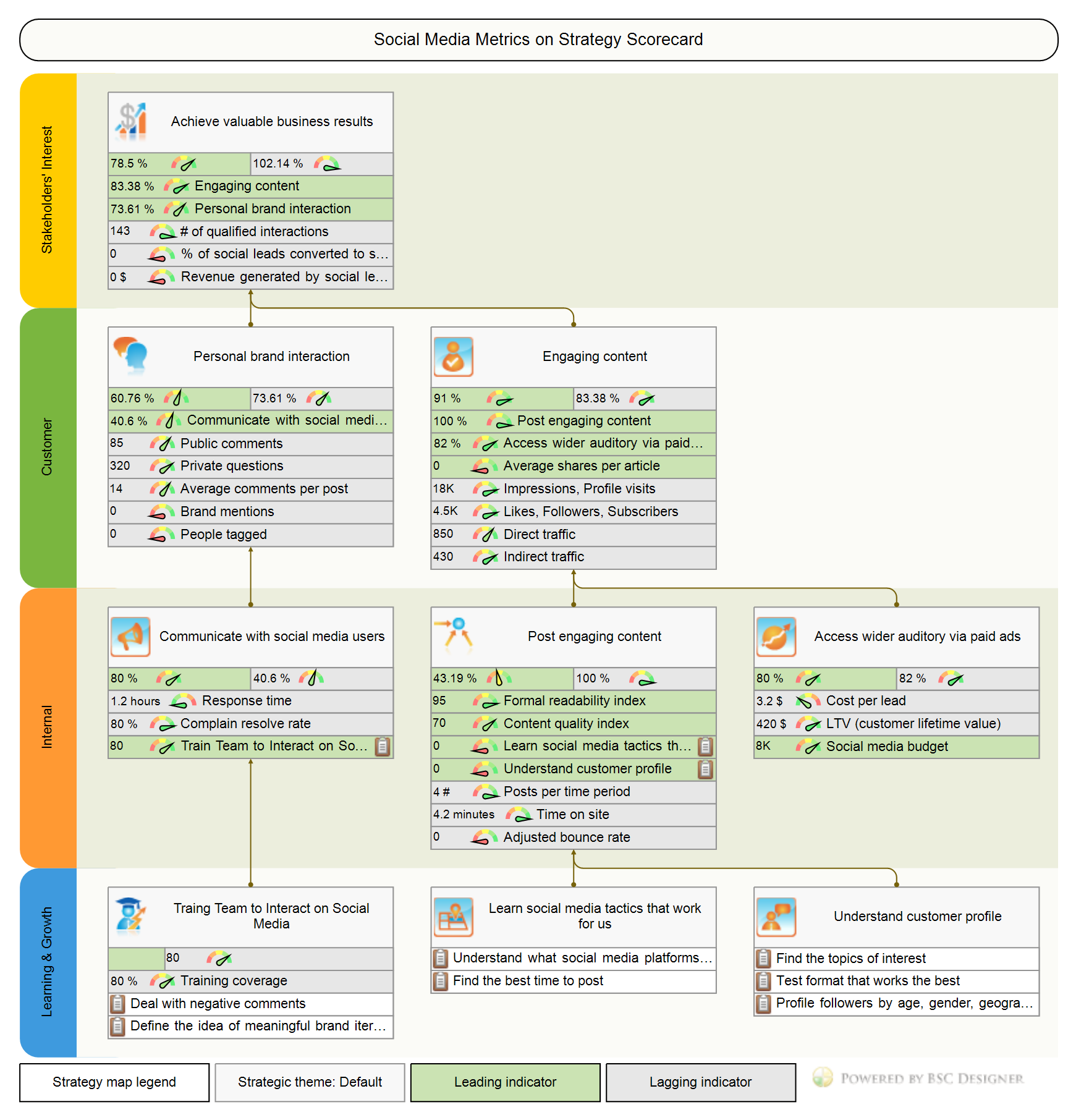

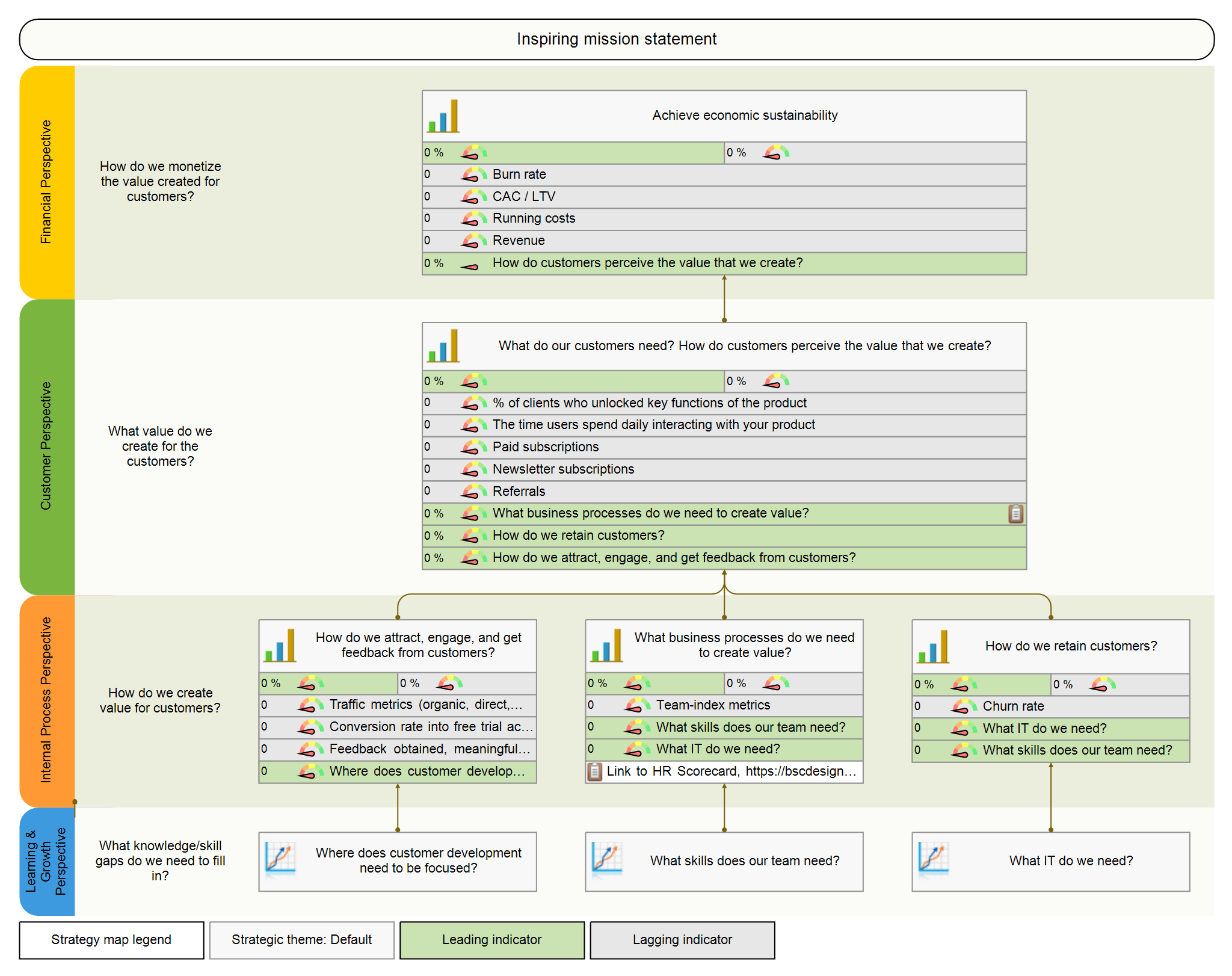

Social Media Strategy Map Example

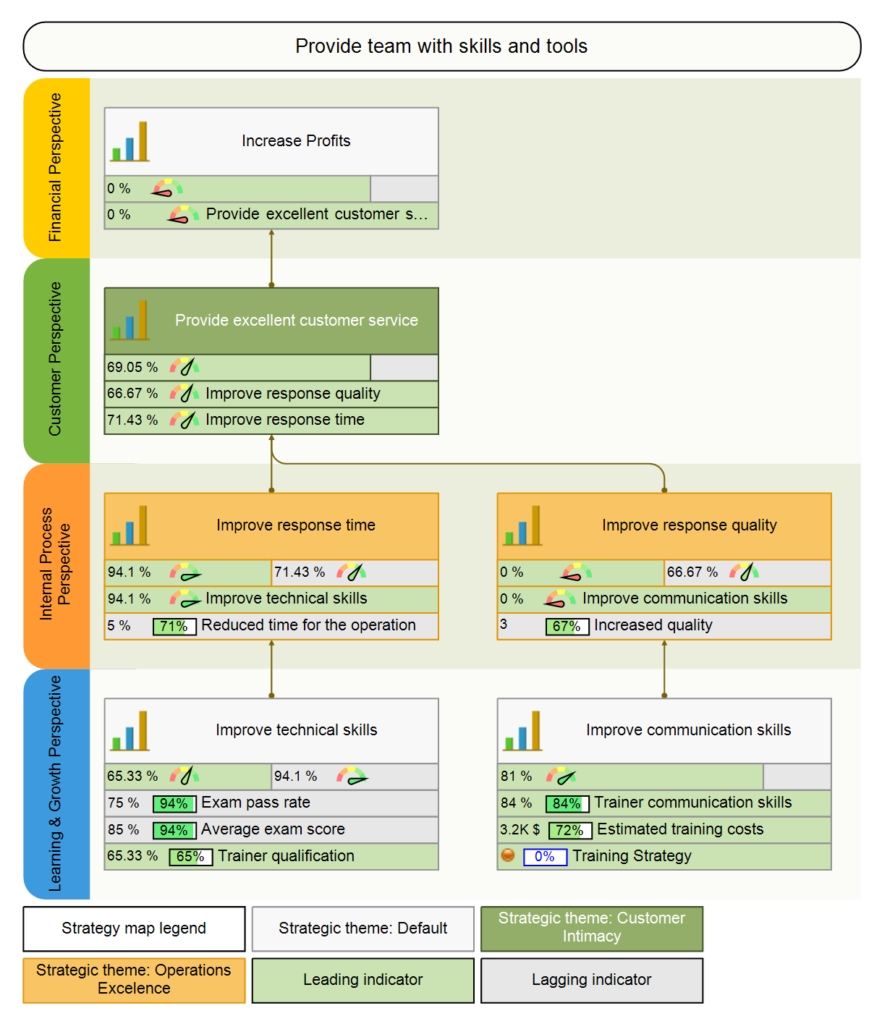

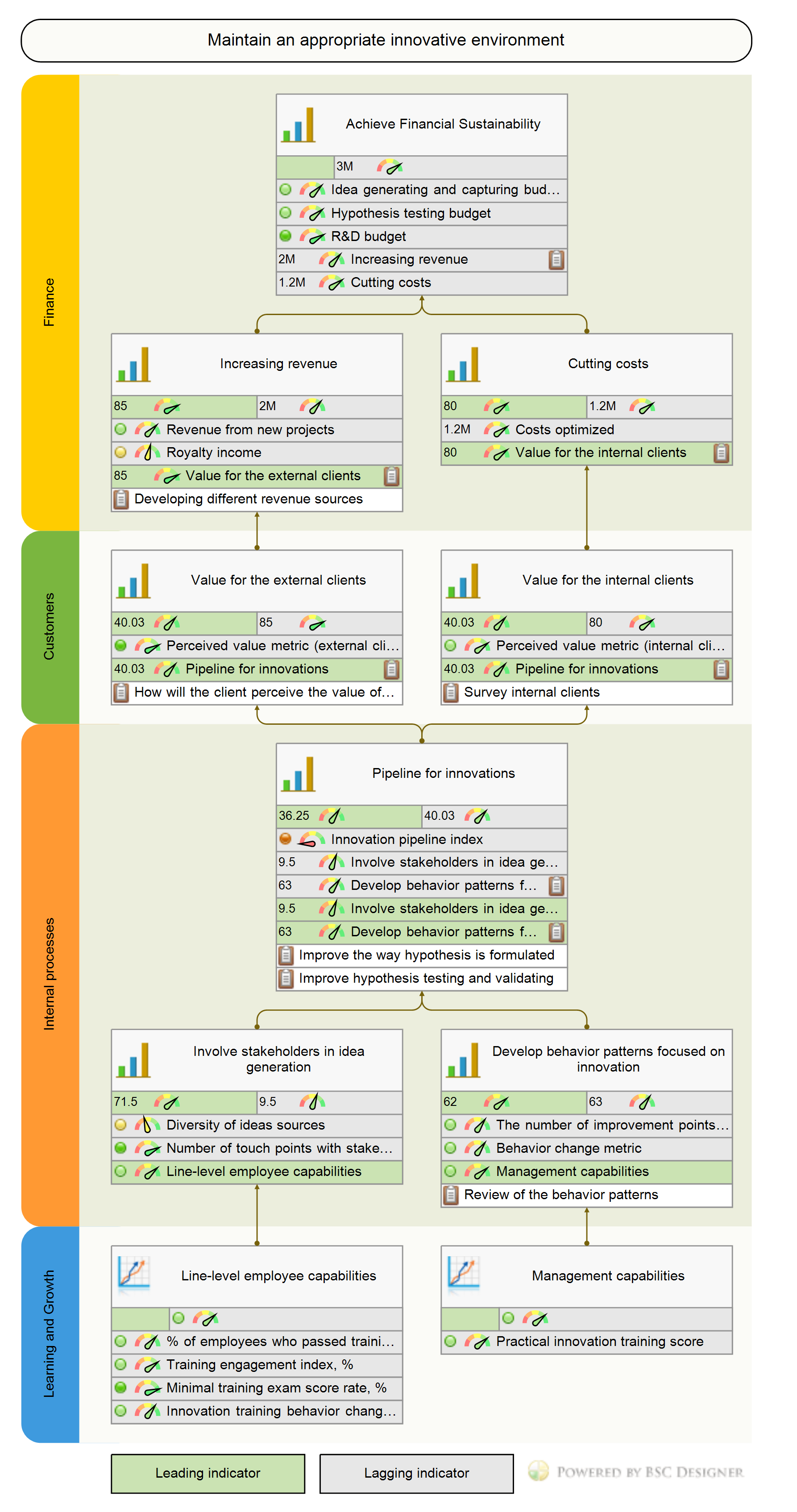

Strategy Map for a Startup

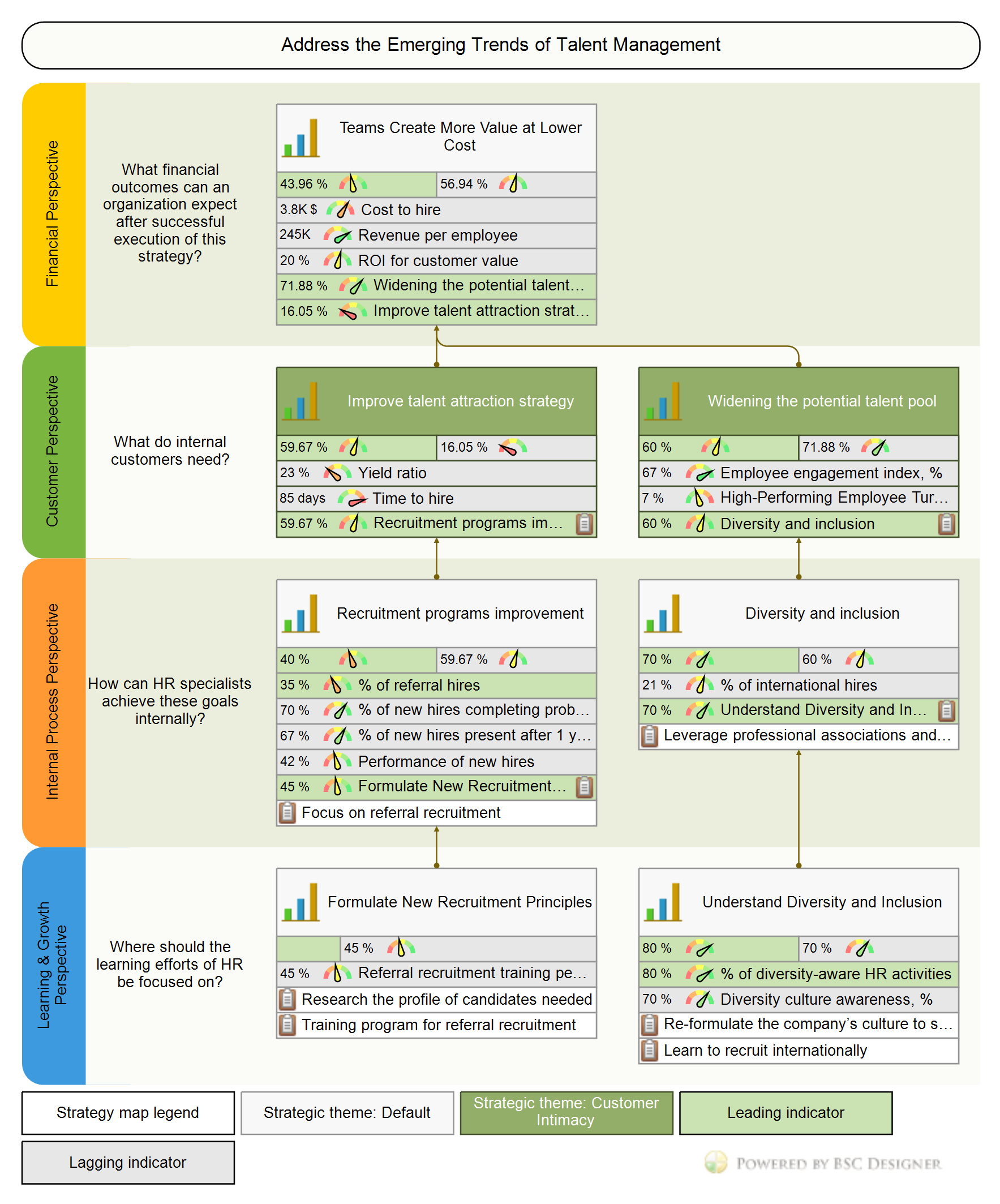

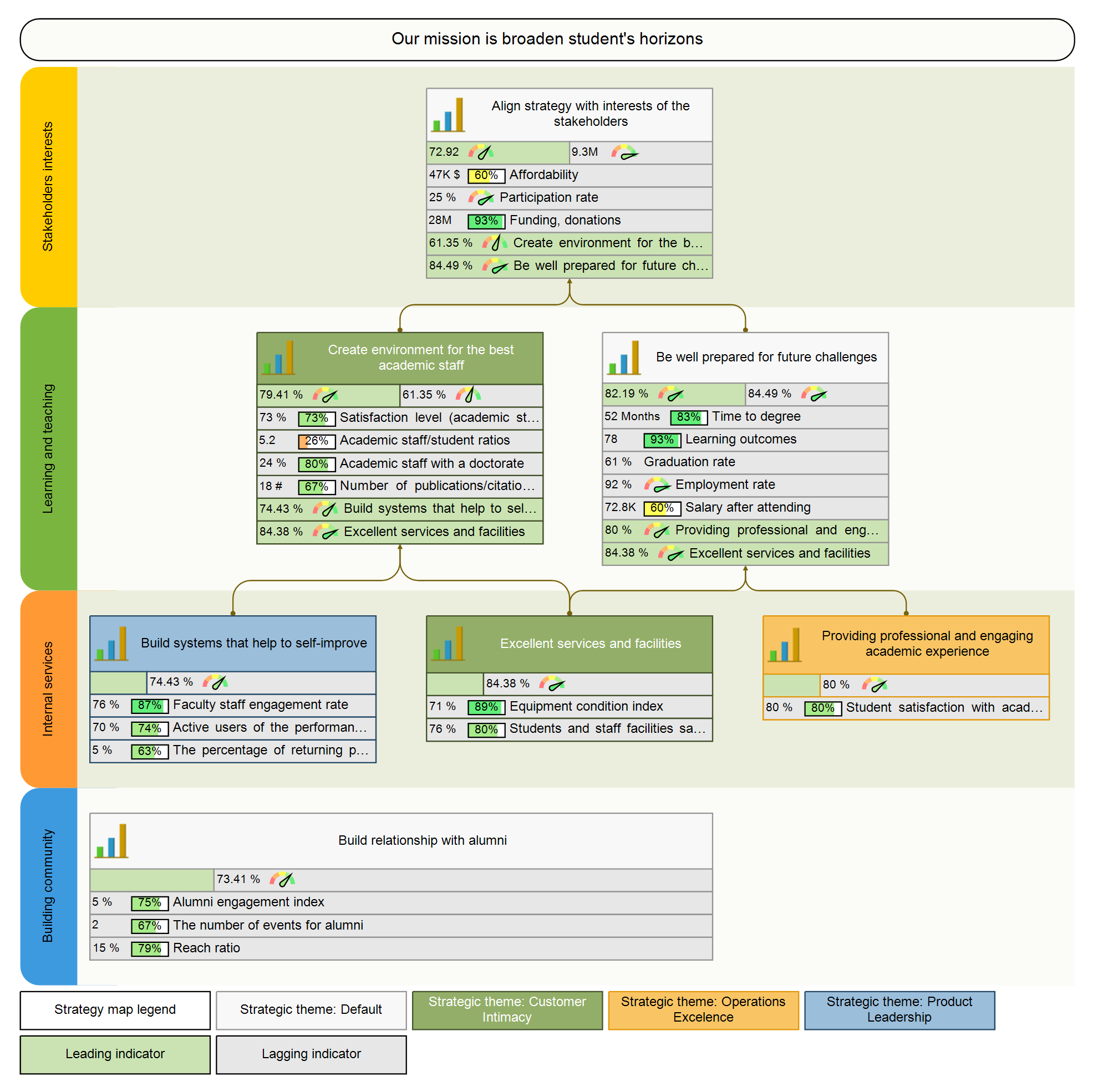

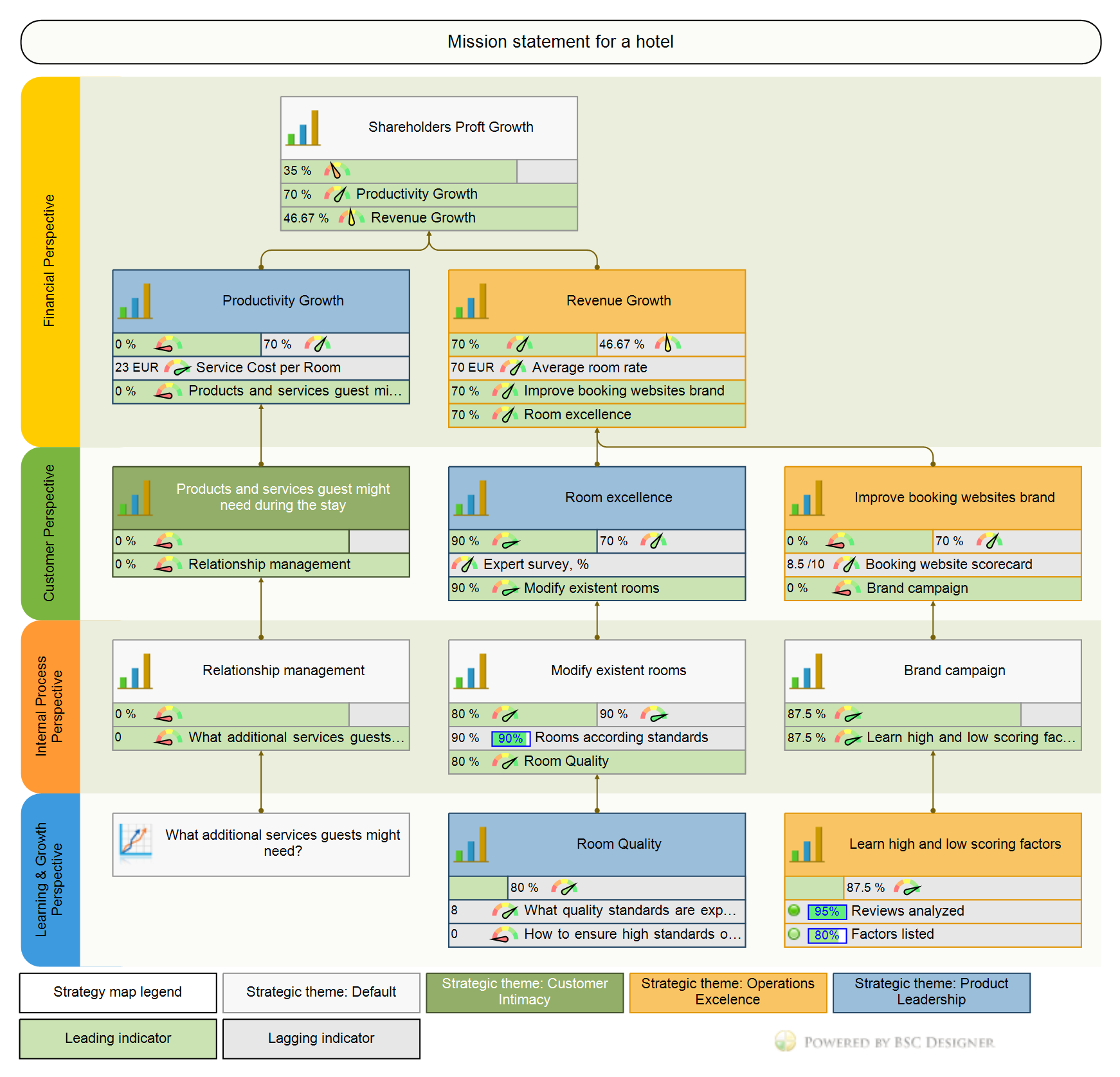

Hotel Strategy Map Example

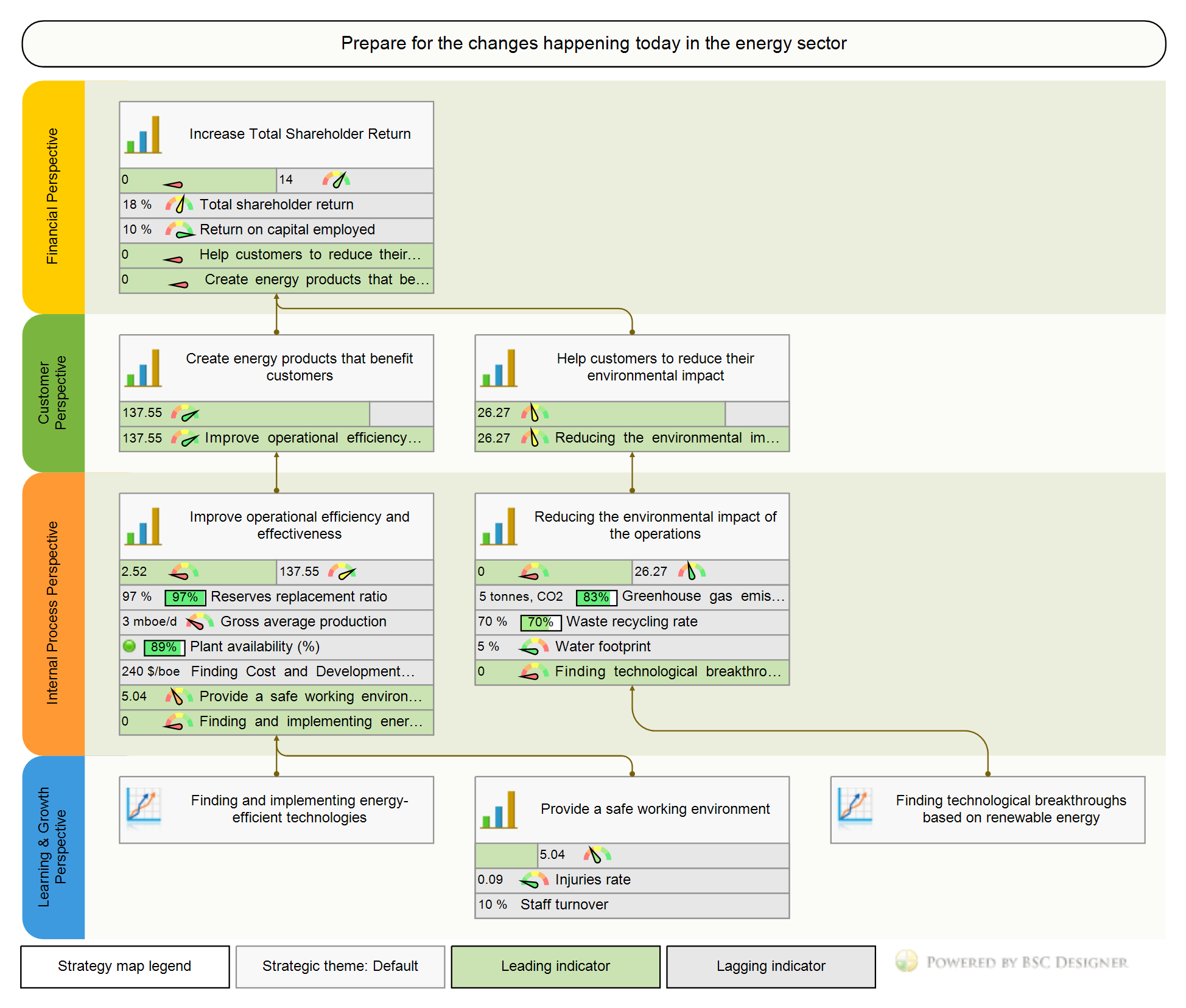

Energy Company Strategy Map

Automation: Drawing Software vs. Strategy Execution Software

Talking about software automation, there are two types of software solutions for the strategy maps design. Let’s call them:

- Drawing tools. That helps to create a nice-looking picture of a strategy map.

- Strategy execution software. Besides creating a visual picture, these tools provide additional automation for KPIs, initiatives, and business goals.

What should you use?

If you are on the prototype stage, or you need a strategy map to simply show it once at the board meeting, then you will be perfectly fine with any drawing tool. Additional information, such as rationale, metrics and their data, action plans, can be presented as a separate document.

If your strategy feels like a marathon, then you need a solution that will support your team from discussion and planning to execution and learning stages. This class of tools is called Balanced Scorecard software, and our BSC Designer is one of the tools recognized by business professionals.

Key Takeaways

- A strategy map is a visual tool that helps with the organization’s strategy on different stages: strategy discussion, description, execution, learning loop.

- We discussed 8 steps that one can follow to create a professional strategy map, as well as typical mistakes that business professional make.

- Choose an appropriate tool for strategy map design: paper template for initial brainstorming, drawing software for presentation, software tools like BSC Designer if you plan to get back to the map during strategy execution.

![]() CEO | Author | Speaker

CEO | Author | Speaker

BSC Designer is strategy execution software that enhances strategy formulation and execution through tangible KPIs. Our proprietary strategy implementation system reflects our practical experience in the strategy domain.

I like it very much. It is very complete ann it has a simple and logical language incluiding for us non english speaking public. Thank you. Orlando Carnota.

Thank you for your expertise! For globalization to BRIC country do you strategize differently regarding manufacturing products?

Having in mind the scope of the article, the approach to the strategy maps it similar in any market. As for strategies themselves, obviously, they need to be tailor made for the company/environment.